YOUR USE OF THIS WEBSITE REQUIRES FULL ACCEPTANCE WITHOUT RESERVATION ON YOUR PART OF THE CONDITIONS OUTLINED BELOW. IF YOU DO NOT ACCEPT THESE CONDITIONS, DO NOT ACCESS THE WEB SITE OR ANY OF ITS PAGES.

Important Information

The content of this website is intended to Professional Investors. If you are a Private Investor, you should ensure to select the correct investor category when you enter this site, as failure to do so may result in you accessing material about investment funds and investment services which may not be suitable for you and/or may not be available for you to invest in.

Limited access

The information provided herein is also intended for Users in territories where it is permissible for Users to access information. This website may indeed contain information about funds established in different jurisdictions and/or investment services offered too. Please consult the specific sections and material to obtain more information. Users are responsible for ascertaining they are legally authorized to consult the information herein and should therefore ensure the investor category chosen to enter this website is correct.

Use of Cookies

Cookies help us collect data about you and how you use our website. For example, we are interested in knowing which internet browser is used, how long you visited the website and which pages you looked at. Information gathered are used to understand how we can improve the design and functionality of our website to better serve you in future. However, if you wish to restrict the cookies set by us or by any third-party sites, you may generally disable cookies in your internet browser. Your browser help function should let you know how to do this. Please keep in mind that restricting cookies may impact your experience and the functionality on this website.

The Interactive Advertising Bureau has produced a guide which explains how cookies work and how they are managed. Please visit www.allaboutcookies.org to read more on this subject.

iMGP Funds Sicav

The data and information featured on this web site are provided free of charge and solely for information purposes. The information contained herein constitutes neither an offer to purchase nor a solicitation to sell and may not be construed as an investment recommendation on the part of iM Global Partner Asset Management or other entities of the group iM Global Partner, its affiliates, managers, officers, or employees (hereafter « iMGP ») and has no legal or contractual value. Furthermore, any reference to a specific security in any published material is included by way of illustrative example and should not be construed as a recommendation to purchase, hold or sell such a security nor does it in any manner constitute the provision of investment advice in relation to same. The iMGP Sicav ( hereafter « iMGP » or « iMGP Funds » or « Fund ») has not taken any measures to adapt to each individual investor who remains responsible for his own independent decisions. Any investment in the funds presented on the web site must be made in conformity with the related legal documentation in force (prospectus, Key Investor Information Documents), as approved, where applicable, by the regulatory authority in your country. iMGP Funds is an open-ended umbrella investment company established and regulated in Luxembourg. The iMGP Sicav is not open to citizens or residents of the USA or to any other party deemed to be a US person. iMGP Funds’ current Prospectus and Key Investor Information Document, by –laws and the Annual and Half Yearly Reports of the Fund can be obtained on this website or from the iMGP offices at 5, Allée Scheffer, L-2520 Luxembourg or from the Agents and Representatives listed on this website for the specific jurisdictions where iMGP Funds are registered and this marketing document is intended for use only in those specific jurisdictions. Investors are advised that they should consult the Prospectus before seeking to subscribe. Moreover, investors are also advised to consult their legal, financial or tax advisors before taking any investment decisions.

Investors are reminded that past performance is not an indicator of future returns, nor does it guarantee future profits, and that they risk, in some cases, losing all or part of the amount initially invested. An investment may increase or decrease by virtue, in particular, of market fluctuations and exchange rate variations in the currency in which the Sub-fund is invested where this differs from the currency of the shareholder.

Disclosure in respect of iM Global Partner Asset Management

Any reference to iM Global Partner Asset Management (« iMGP AM ») or iM Global Partner (« iMGP ») in the material published on this website should be construed as being a reference to one or more of the legal entities, listed below, dependent on the particular jurisdiction in which it is being accessed.

iMGP AM is the Luxembourg management company of iMGP Funds

iMGP is a French regulated entity which represents and distributes iMGP Funds that have been registered in France having branches in Italy, Spain, Germany and also subsidiaries in Switzerland and in the UK for that purpose. iMGP AM is also a subsidiary of iMGP.

Use of links

This website may direct you to automatic links to other websites. Use of these links is made at your own risk. iMGP and the Fund will not have developed, verified the accuracy or scrutinised the data contained in the aforementioned links. iMGP and the Fund may not be held responsible for damage or losses caused by delays, defects or omissions that may exist in the real, indicated or indirect services, information or other content provided on this site. iMGP and the Fund give no guarantee, makes no declaration and will not be held responsible for any content transmitted by electronic means to a third party, including the accuracy, subject, quality or the appropriate character of said content.

Copyrights and Trademarks

The entire content of this website is subject to copyright with all rights reserved to iMGP and the Fund. You may download or print out a hard copy of individual pages and/or sections of the website, provided that you do not remove any copyright or other proprietary notices. Any downloading or otherwise copying from the website will not transfer title to any software or material to you. You may not reproduce (in whole or in part), transmit (by electronic means or otherwise), modify, link into or use for any public or commercial purpose the website without the prior written permission of iMGP.

Please select your country

Which best describes you?

Individual Investor

Non-investment professionals who are researching investments for their personal accounts (from small ISA investors through to “high net worth” individuals).

Investment Professional

Investment professionals who provide investment advice to their clients (“advice-givers”).

Institutional

Investment professionals who manage money on a discretionary basis on behalf of others (“money managers”) or who perform fund or manager research.

I confirm that I have read and agreed to the Terms & Conditions and that I meet the applicable investor requirements for my jurisdiction.

An investment strategy that seeks trends across commodity, rates, currency, and equity markets.

Managed

Dynamic and tactical approach, not static

Futures

Takes long and short positions using futures contracts

Quant

Humans build models, models determine portfolios

Trends

Durable source of alpha based on prices, not macro calls

Andrew Beer (co-portfolio manager of DBMF) explains managed futures

What can managed futures do for your portfolio?

An incredibly valuable portfolio diversifier to stocks and bonds

Long-term returns

Source: Bloomberg. DBi. Data from 3rd January 2000 to 31st December 2025, net of fees. Data refers to cumulative past performance. Cumulative past performance is not a reliable indicator of future results. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index.

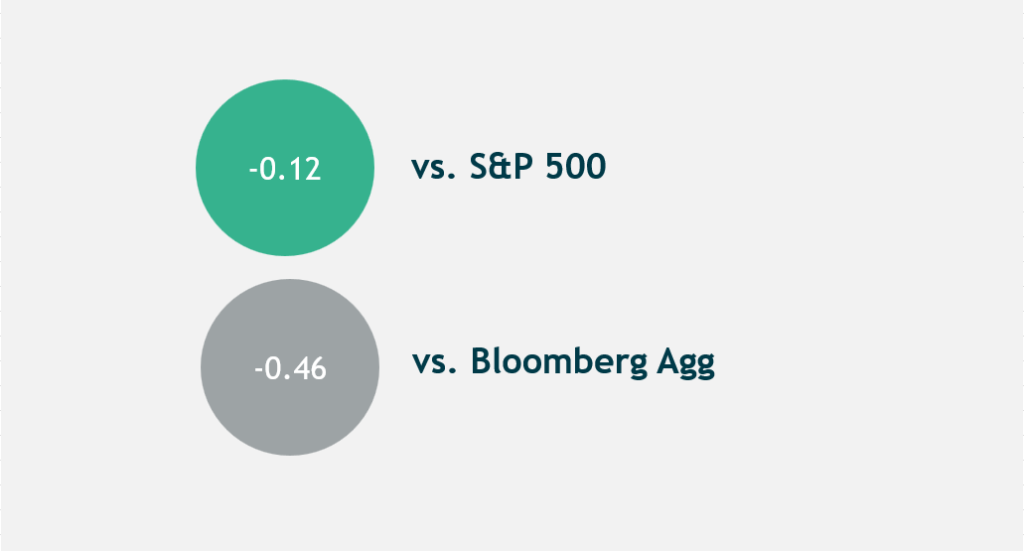

Low correlation to traditional asset classes

Source: Bloomberg. DBi. Data from 3rd January 2000 to 31st December 2025, net of fees. Data refers to cumulative past performance. Cumulative past performance is not a reliable indicator of future results. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index.

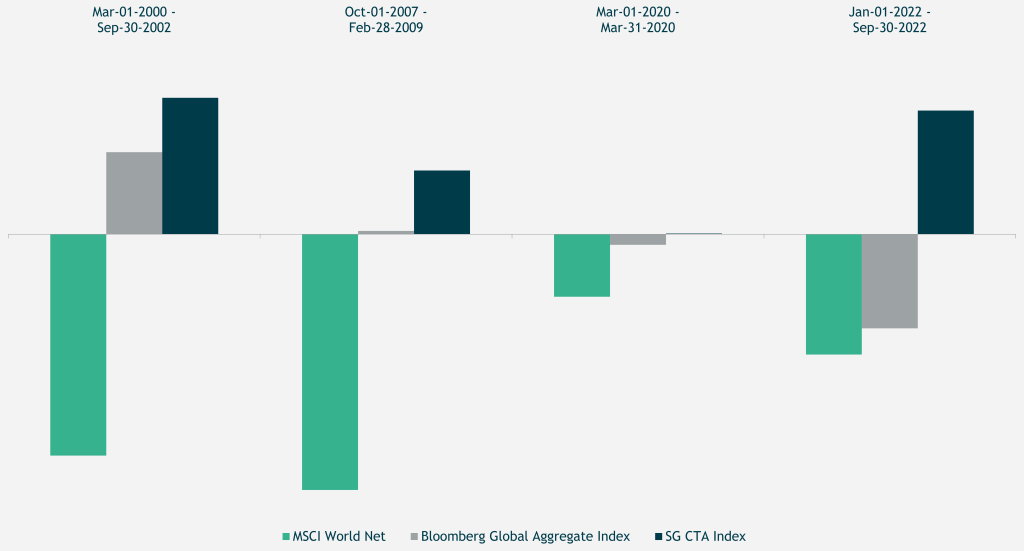

Alpha during prolonged crises

Source: Bloomberg. DBi. Data from 3rd January 2000 to 31st December 2025, net of fees. Data refers to cumulative past performance. Cumulative past performance is not a reliable indicator of future results. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index.

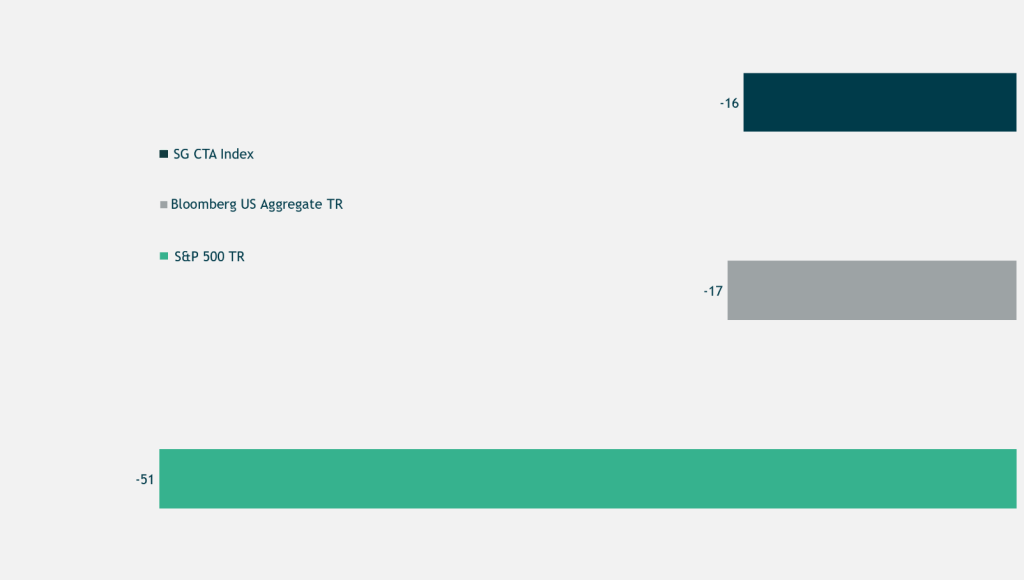

Max drawdown significantly lower than traditional asset classes

Source: Bloomberg. DBi. Data from 3rd January 2000 to 31st December 2025, net of fees. Data refers to cumulative past performance. Cumulative past performance is not a reliable indicator of future results. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index.

Managed futures & DBMF: The essential alternative asset class

Why DBMF ?

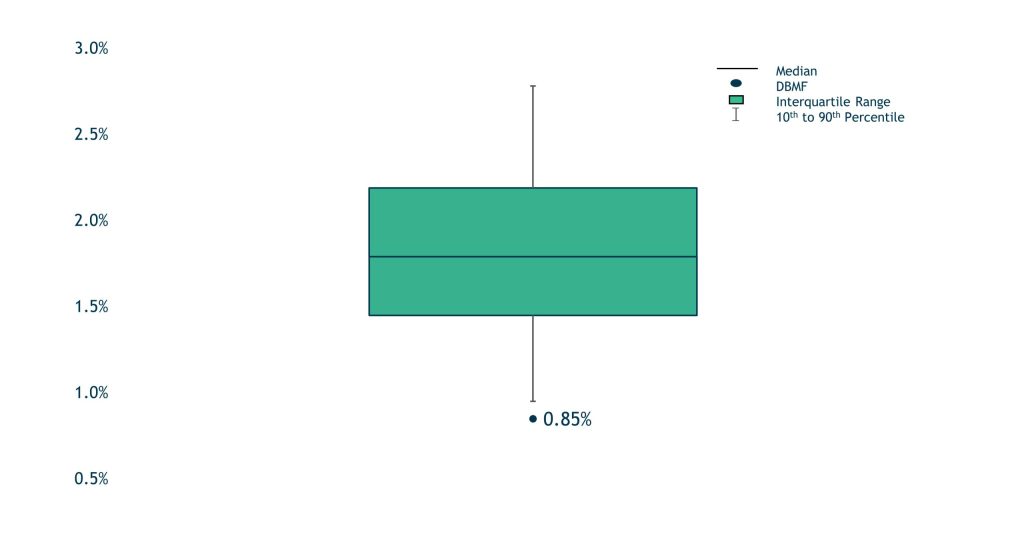

One of the lowest fees in the category

85 bps

DBMF expense ratio is at the bottom decile of peers

Net expense ratios in the Morningstar Systematic Trend category

Source: Morningstar, eVestment, DBi. Cumulative past performance is not a reliable indicator of future results. As of March 31st 2026, net of fees, since inception (5/7/19). This is an active ETF which is not managed in relation to any benchmark. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index. Past results are not indicative of future results.

Aims to reduce risk of materially underperforming benchmark

80%

Confidence tracking to index

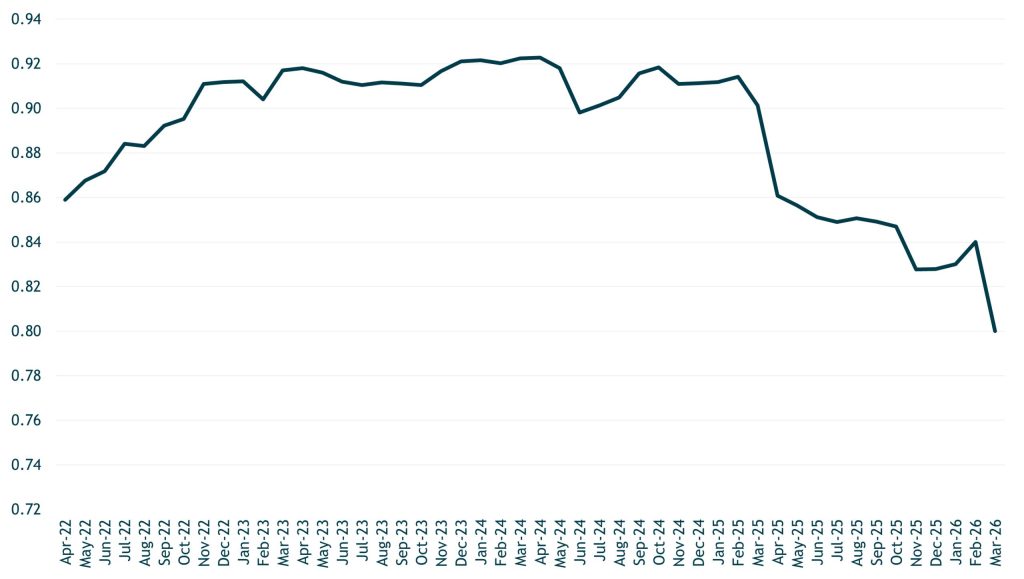

SG CTA index correlation to DBMF (NAV)

Source: Morningstar, eVestment, DBi. Cumulative past performance is not a reliable indicator of future results. As of 31th December 2025, net of fees, since (4/01/22). This is an active ETF which is not managed in relation to any benchmark. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index. Past results are not indicative of future results. Investment correlation measures how different assets move in relation to each other. A perfect correlation of +1 means both asset prices move in the same direction (go up together, and go down together). A correlation of -1 indicates they move in opposite directions.

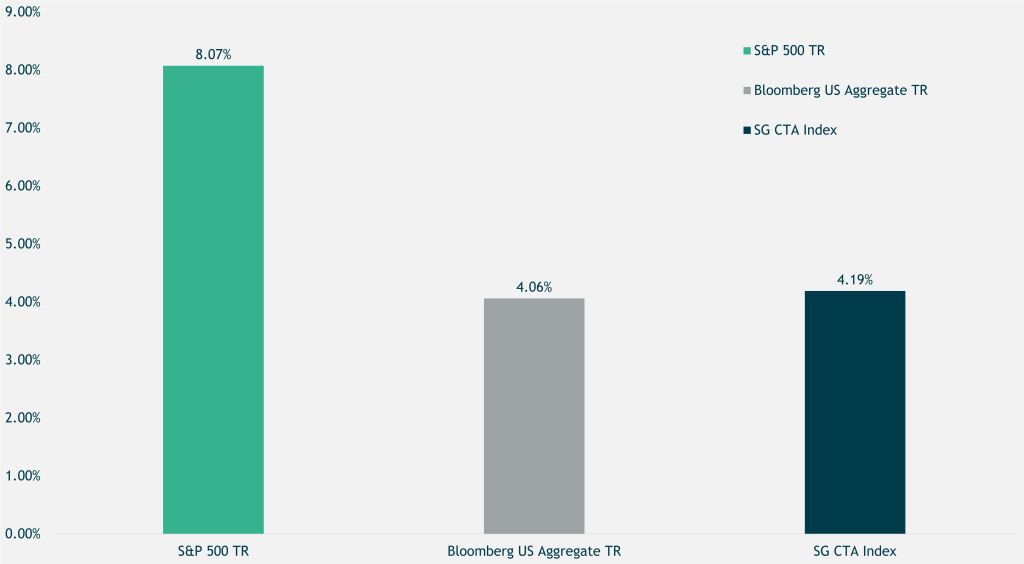

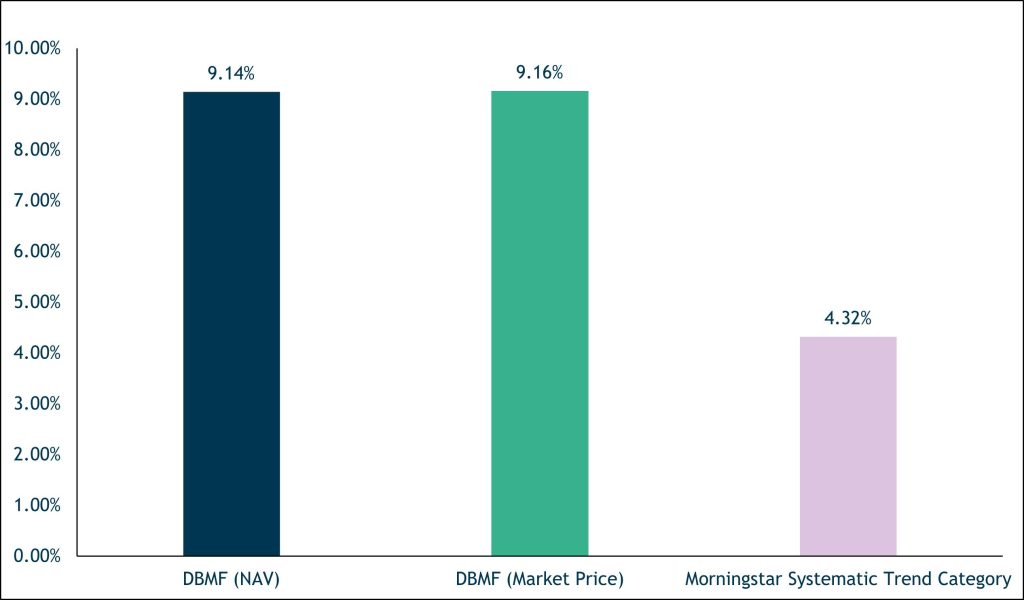

History of outperforming index

+8.64

DBMF has delivered returns over category for 5 years

Annualised returns since DBMF inception

Source: Morningstar, eVestment, DBi. Cumulative past performance is not a reliable indicator of future results. As of March 31st 2026, net of fees, since inception (5/7/19). This is an active ETF which is not managed in relation to any benchmark. This data is being shown for illustrative purposes only. The index is not representative of the entire population of CTAs or hedge funds. The index’s performance may not be indicative of any individual CTAs or hedge funds. The index may not have been adjusted for fees/commissions. The index cannot be traded by individual investors. The actual rates of return experienced by investors may be significantly different and more volatile than those of the index. Past results are not indicative of future results.

DBi’s approach to managed futures

The iMGP DBi Managed Futures Fund seeks to replicate the pre-fee performance of a representative basket of leading managed futures hedge funds.

Investment strategy

The iMGP DBi Managed Futures Fund seeks to replicate the pre-fee performance of a representative basket of leading managed futures hedge funds.

Factor analysis is used to determine the current positions of the managed futures hedge funds.

The positions are then replicated using highly liquid futures contracts in equity, fixed income, currencies and commodities.

This approach is a smart and efficient way to gain exposure to managed futures, with the aim of outperforming the representative basket by 300-400 bps per annum, net of fees.

Through this strategy, the fund aims to mitigate three key investment risks:

Concentration Single Manager, Single fund, industry, geography

Human Biases Selection bias, etc.

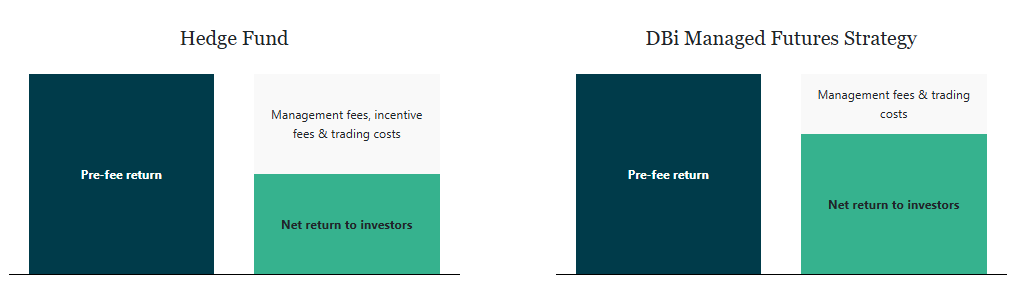

Fee reduction is the purest form of alpha

The strategy seeks to optimize net returns to investors by approximating the main exposures that drive performance, minimizing trading and implementation costs, and offering lower all-in fees.

DBi’s Strategies seek to outperform by delivering 80-100+% of pre-fee hedge fund returns with lower fees and expenses.

iMGP DBi Managed Futures Strategy ETF Update with Andrew Beer | January 2026

Andrew Beer & Mike Pacitto dive deep into comparing managed futures to all major asset classes in terms of historical performance, alpha-generation, drawdowns, Sharpe, etc.

The strategy is an extremely effective diversification tool for traditional portfolios. It has no long-term structural correlation to stocks, bonds, or commodities (because it can be long or short any market based on prevailing price trends). Adding managed futures has historically reduced portfolio volatility without significantly reducing expected returns, producing a smoother ride. Additionally, the strategy has historically produced attractive absolute returns during extended periods of losses for traditional assets, also known as “crisis alpha.”

Almost every other managed futures fund is an active strategy based on the manager’s models, primarily for capturing trends in different asset classes, usually using more than 50 or even 100 futures markets. Some managers may also include non-trend models (e.g. carry) to varying degrees. DBMF is based on replicating the (gross, pre-incentive fee) performance of the SG CTA Index, which is comprised of 20 of the leading managed futures hedge funds. DBMF’s model uses the daily returns of the index to create a portfolio highly correlated to the index, using only 10-15 of the most liquid futures contracts. By tracking 20 leading funds via the index, DBMF eliminates the “single manager risk” of being invested in only one fund that underperforms the index dramatically and/or over an extended period.

It is a passive strategy in the sense that it is model-based and attempts to replicate an index, but the “index” itself is comprised of 20 active managers. Also notable, the “index” includes the underlying fees of the active managers. DBMF seeks an “index-plus” outcome by extracting fees from the index it replicates.

Yes, the fund earns interest on the collateral portfolio (typically 3-month T-bills), which is distributed quarterly. Capital gains are distributed annually.

Because managed futures bring strong diversification benefits to a portfolio, based on the statistics, you should hold about as much in managed futures as you can confidently defend when the strategy isn’t performing well. (Almost no one allocates as much as an optimizer would suggest, which is typically about 25-50% of a portfolio, depending on a number of factors.) Despite the significant long-term benefits, managed futures can sometimes be frustrating for extended stretches. Sizing an allocation appropriately is critical: the allocation should be big enough to move the needle in your portfolio when it’s working, otherwise the inevitable challenging periods along the way will hardly be worth it.But the allocation can’t be so big that you (or your client) will throw in the towel during rough patches. The best asset allocation is one that you can stick to for the long term, including through down periods for every component asset class or strategy. Every situation is different, but we think an allocation to managed futures in the 5% to 10% range is the practical sweet spot for most balanced portfolio investors (although higher allocations are well supported by the statistics).

Because managed futures have essentially no long-term correlation to anything, it makes sense to fund them pro rata from an existing allocation. The existing allocation has presumably been “optimized” for the investor’s return goals and risk tolerance based on the performance and correlation characteristics of its underlying components. Funding pro rata from these sources should preserve the expected return profile of the portfolio’s core, while adding the diversification benefits and (likely) crisis alpha of managed futures.A reasonable case could also be made to fund an allocation more than pro rata from bonds, given stocks outperform bonds over long time horizons, and managed futures tend to perform well during extended stock market weakness (i.e., periods of weeks to months, not days to weeks). The “optimal” allocation depends on what is being optimized (risk-adjusted returns, expected maximum total return, etc.). For a client that is more concerned with risk from a specific asset class, or has some other consideration, the funding sources could of course be customized further according to individual circumstances.

Managed futures strategies are heavily (sometimes solely) based on trend following, a strategy that dates back hundreds of years, but is today executed by sophisticated managers with vast amounts of computing power to build and refine quantitative models.While the details and execution are complex, the underlying premise is simple: across equity markets, bond markets, commodities and currencies, go long assets/markets that are rising in price, and go short assets/markets that are falling in price, using liquid futures contracts to gain exposure. There are numerous theories addressing why trend following works, including divergent economic fundamentals across countries and industries, supply-demand dynamics, market structure, and investor psychology.Regardless of the “correct” explanation, over its history, trend following has produced positive returns with essentially zero long-term correlation to traditional asset classes, and has tended to perform best in extended bear markets for stocks and bonds.DBMF is a simple, cost-effective way to add the benefits of managed futures to a portfolio without the risks of choosing a single manager whose style may be out of sync with markets in any given month, quarter, etc.

Book a meeting with the iMGP team to explore

the potential of DBi Managed Futures!

An error has occurred, please try again later.An error has occurred, please try again later.

×

You are now leaving iMGP.com

You are about to leave our website and visit an external site. iMGP is not responsible for the content, security, or privacy practices of external websites.