The conflict between the U.S. & Israel and Iran has now entered its second week. Heightened geopolitical risk combined with renewed inflation concerns linked to higher energy prices led both bond and equity markets to decline last week: Crude oil prices have risen sharply from around $70/bbl to nearly $100/bbl following the closure of the Strait of Hormuz, through which approximately 20% of the global oil supply transits each day. As of 9th March, global equities had declined by around 3.8% in USD month to date, while U.S. sovereign bonds were down 0.7%. Energy equities were among the few sectors delivering positive returns, rising 1.5% month to date.

With the intensity of the conflict appearing to moderate following the initial escalation, the main question for markets is how long will it persist. There are relatively few assets capable of protecting portfolios during the kind of sharp, short-lived drawdowns seen last week, aside from short-selling or the use of portfolio insurance. Historically, markets tend to recover quickly from initial geopolitical shocks provided the disruption does not translate into sustained economic damage. Examples include the imposition of tariffs in 2025, or the initial market reaction during the COVID pandemic market crash of 2020.

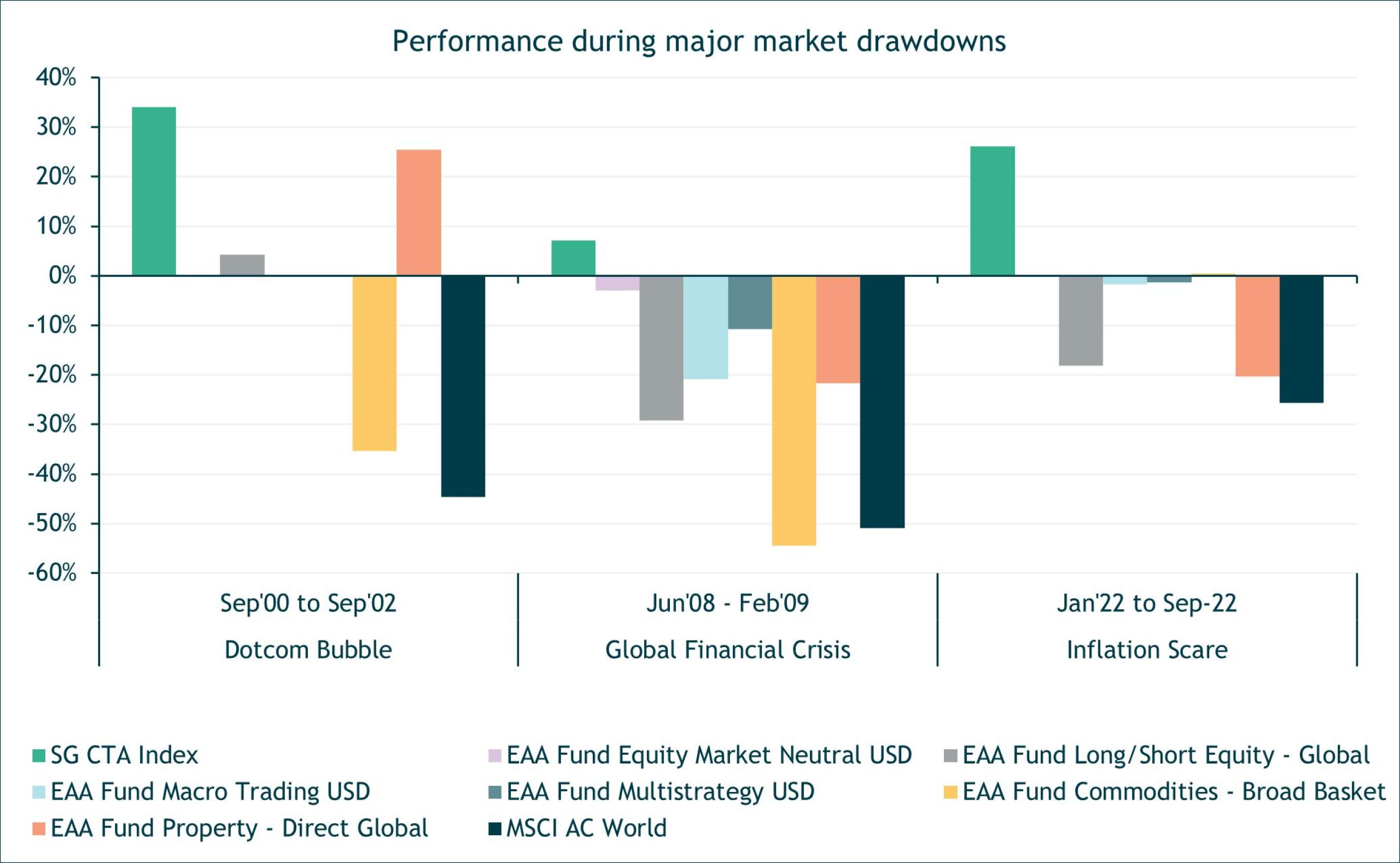

The real damage to portfolios is done during extended drawdowns, where risk assets experience deeper and more persistent declines. Such periods include the bursting of the Dot-Com bubble in 2000, the Great Financial Crisis of 2008, or more recently the Inflation-driven sell-off of 2022.

In these periods true portfolio diversifiers become particularly valuable. Managed Futures strategies (as indicated by the SG CTA Index below) have historically generated strong positive returns when other diversifying assets have struggled alongside equities.

Source: Bloomberg, Morningstar, iM Global Partner as of March 2026

Against a backdrop of elevated geopolitical uncertainty, what is certain is that the odds of a tail-risk scenario have increased, and the case for portfolio diversification has never been stronger.