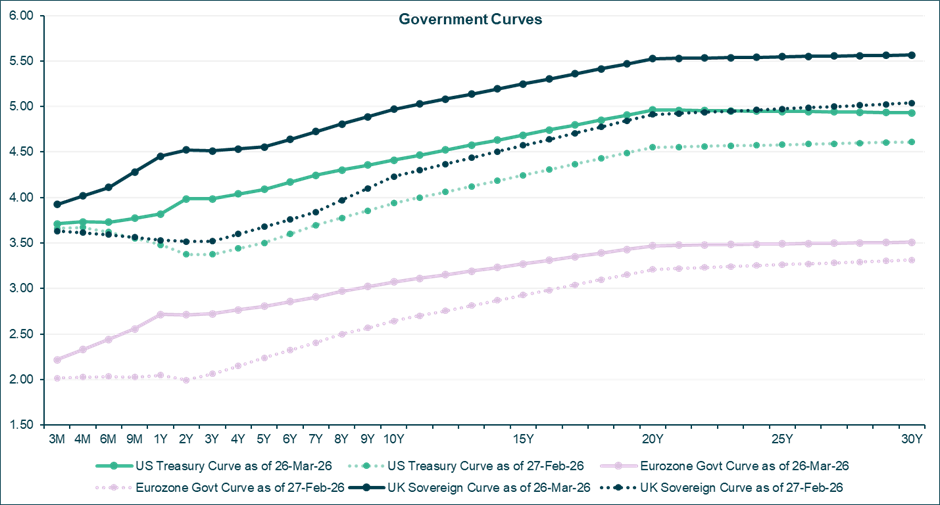

The threat of energy-driven inflation has unsettled global fixed income markets, with interest rates rising sharply since the end of February, by around 50-60bps in the US and Eurozone, and over 80bps in the UK.

Source: iMGP, Bloomberg as of 30 March 2026

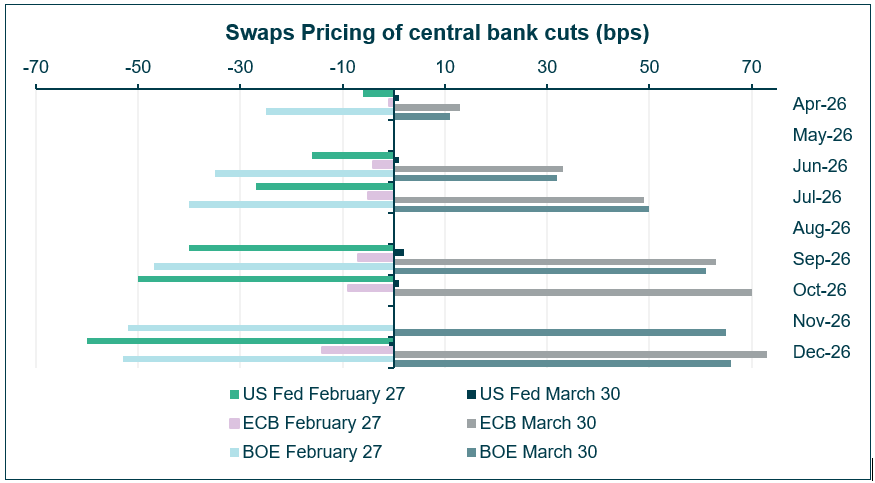

At the same time, markets have dramatically revised their expectations for central bank policy. Investors now anticipate that the Federal Reserve will deliver no rate cuts for the remainder of the year (compared with expectations of two cuts at the end of February). In parallel, both the Bank of England and the European Central Bank are now expected to deliver two interest rate hikes, a notable shift from earlier expectations of easing.

Source: Bloomberg as of 30 March 2026

We are somewhat sceptical of the scale of this repricing. The recent rise in yields may represent an attractive entry point for yield seeking investors, particularly as both a rapid resolution and a more prolonged conflict in the Persian Gulf could result in the need for interest rate cuts.

In the shorter-duration scenario, the recent increase in energy prices driven by the disruption to supply through the Strait of Hormuz is likely to be short lived or ‘transitory’ in central bank speak. Central banks tend to focus on core measures of inflation which exclude more volatile components such as energy (including Core Personal Consumption Expenditures (PCE) in the U.S., and Core Harmonised Index of Consumer Prices (HICP) in the Eurozone). so we find it unlikely that a shorter duration shock in an element of inflation which is purposely excluded from their core focus would result in interest rate hikes.

A more prolonged conflict and subsequent higher structural energy prices would likely weigh on economic activity via higher input costs and weaker demand. In such an environment it seems hard to fathom that central banks would raise rates to fight an inflationary force they cannot control; and are much more likely to lower rates in order to stimulate the economy.

The good news for investors is that the rise in interest rates has improved the attractiveness of fixed income markets. In the U.S., intermediate term (1-10yr) investment grade corporate bonds are now yielding 4.9%, 1and in Europe the equivalent bonds yield 3.7%2For investors seeking more yield, global high yield bonds will generate 7.3%3 yield and European high yield 6.0%4.