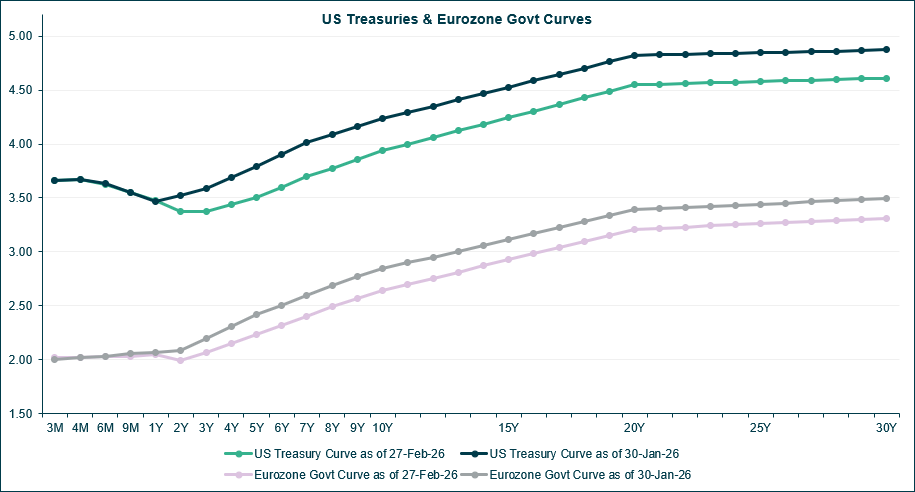

After a quiet start to 2026, interest rates fell in February in both the U.S. and Europe, as declining inflation data increased the likelihood of interest rate cuts in the United States (markets continue to believe the ECB will remain firmly on hold). The falling rates contributed to strong performance over the month, with the Bloomberg U.S. Corporate Total Return Unhedged Index gaining 1.3% in February, and the Bloomberg U.S. Intermediate Credit Index rising 1.0%. European credit underperformed its U.S. counterparts as a result of smaller rate movements within the Eurozone, with the Bloomberg Euro Aggregate Corporate Total Return Index returning 0.6% in EUR terms in February.

Source: iMGP, Bloomberg, as of 27 February 2026

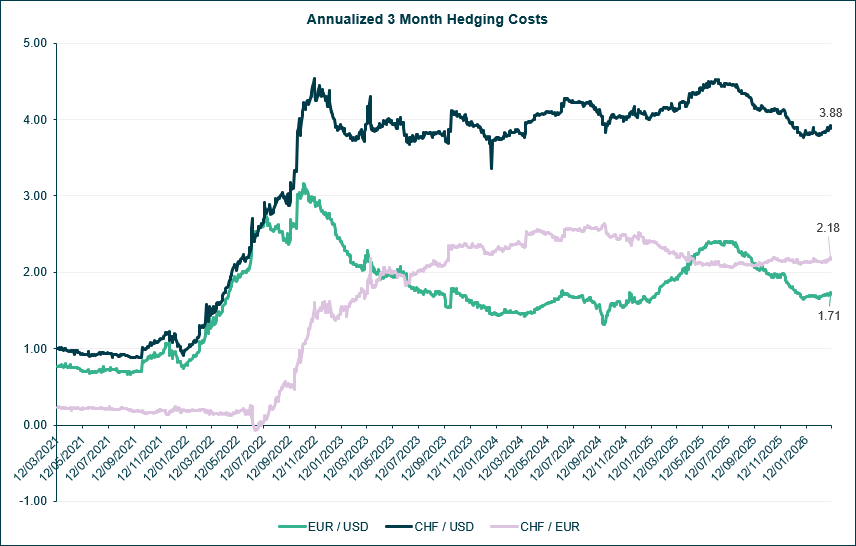

Hedging rates from USD into euros and Swiss francs were stable throughout February but have crept up month-to-date in March, due to the impact of the spike in oil prices on future inflation expectations. Despite the renewed conflict in the Persian Gulf, markets continue to predict that the U.S. Federal Reserve will keep cutting rates throughout 2026, while the ECB is currently forecast to remain on hold. This narrowing of interest rate differentials between the U.S. and Europe/Switzerland should result in a fall in hedging rates, making USD-denominated investments more attractive for euro- and franc-based clients.

Source: iMGP, Bloomberg, as of 11 March 2026

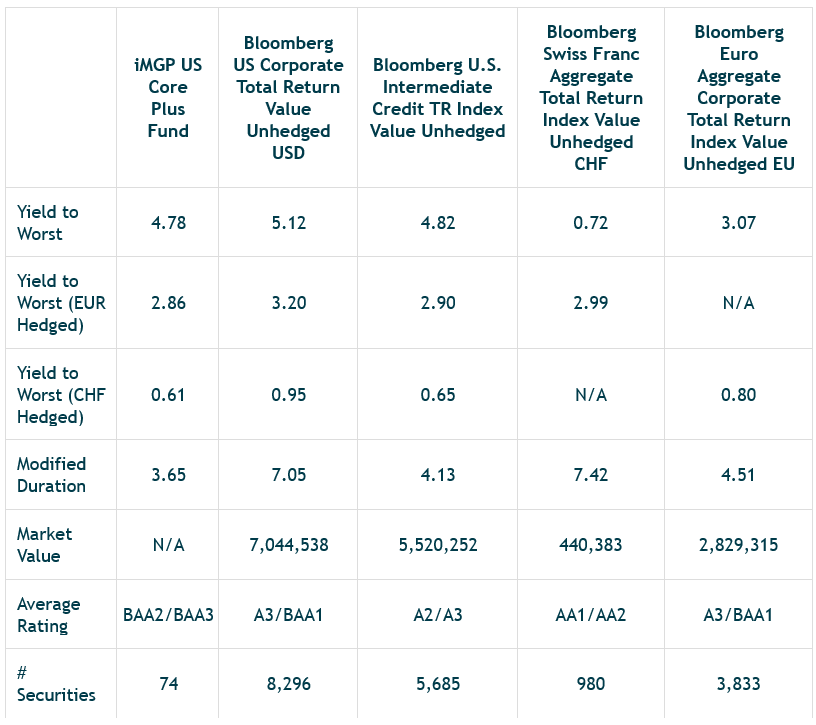

The iMGP US Core Plus Fund continues to be positioned cautiously; however, careful selection of credit has allowed the portfolio to produce yields at similar levels to longer-duration benchmark indices. We believe that U.S. intermediate-term credit currently offers a compelling absolute level of yield, particularly relative to pre-pandemic averages. For European investors, the additional benefit of declining hedging rates further enhances the potential attractiveness of this asset class, which offers both diversification opportunities and appealing yield levels. Looking ahead to 2026, the fundamentals supporting the strategy remain attractive, underpinned by strong corporate earnings, robust investor demand, and the anticipated easing from the U.S. Federal Reserve.

Past performance does not predict futures returns

Source: iMGP, Bloomberg, as of 27 February 2026