Key insights:

- While Polen Capital pursues overall financial objectives comparable to those of its peers, the path it takes to achieve them – through a more balanced and resilient portfolio construction – sets it apart as a truly distinctive proposition.

- Importantly, this is achieved without compromising its high-conviction approach, reflected in the most selective portfolios in its category.

- Such positioning may offer a strategic edge should the market broaden its focus beyond the current dominance of a few large-cap growth stocks.

High levels of concentration in the US equity market over the past few years have resulted in a handful of companies, particularly the technology giants known as the Magnificent 7, driving the bulk of investment returns. While some investors have benefited from exposure to these companies in their portfolios, their dominance in the US equity market also creates risks.

Polen Capital’s Focus Growth strategy stands out among its peers with a distinctly balanced approach to security weighting. This framework helps mitigate the risks associated with the elevated market concentration currently being observed. While the strategy’s benchmark-agnostic approach has resulted in near-term underperformance as market concentration has intensified, we believe that Polen’s approach remains a compelling way to gain exposure to US quality growth companies over the long term.

In addition to our existing due diligence and monitoring of the company, our view is supported by a quantitative analysis of the Polen Focus Growth strategy and the 30 largest funds in the Morningstar US Large Cap Growth category. All calculations reported herein were performed by iMGP based on data extracted from FactSet and Morningstar as of the end of August 2025.

Selective stance, robust portfolio structure

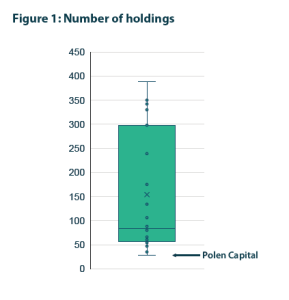

A close look at portfolio composition illustrates how Polen’s approach differs from its peers. Figure 1 shows the distribution of the number of holdings across individual funds.

The median and average number of holdings stand at 84 and 154, respectively. With just 28 holdings in the Focus Growth strategy portfolio, Polen is the highest-conviction manager in the peer group. However, this does not mean the strategy has the most skewed weighting profile; in fact, the data that we are examining in this article show the opposite.

Figure 2 shows the individual weights of the 28 largest positions within the benchmark (dark blue), the median of the peer group (light purple), and Polen’s strategy (turquoise). Polen’s team allocates less to its top two to three holdings compared to the benchmark and its peers. Instead, they assign relatively higher weights to the rest of the strategy’s holdings. The distribution of holdings by their weightings appears significantly more compact in Polen’s strategy.

To quantify portfolio concentration levels, the breadth indicator¹ is applied to the holdings of each portfolio in the sample. This metric encapsulates the idea that a portfolio allocating 10% to each of nine companies, and 0.1% to 100 others, behaves as if it was invested in just nine effective holdings. Figure 3 shows that, although Polen holds by far the smallest number of holdings (28), its effective number of holdings (21) aligns with the median observed across the full fund universe (21) and even exceeds that of the benchmark (18). In other words, 21 of Polen’s 28 holdings are effectively significant, resulting in a diversification ratio of 75%.

As Figure 4 shows, Polen has the highest diversification ratio, indicating the lowest portfolio concentration among the selected holdings. The average and median ratios across the peer universe stand at 26% and 23% respectively, while the benchmark’s ratio reaches only 5%.

1. The breadth indicator is computed as the inverse of the Herfindahl-Hirschman Index (HHI), which itself is derived by summing the squares of the market shares of each holding in theportfolio. The Herfindahl-Hirschman Index is widely used in antitrust analysis to assess the level of competition within industries.

Such a high diversification ratio results in an underweighting – relative to peers and the benchmark – of the stocks with the largest market capitalisations. Meanwhile, Figure 5 (above) shows that Polen ranks lowest in terms of exposure to Nvidia and the Magnificent 7 stocks.

Mitigating stock-specific outcome risk without compromising portfolio financial profile

At the heart of Polen’s approach lies a clear ambition: harness multiple growth levers across the portfolio. Polen’s investment philosophy emphasises long-term fundamentals, selecting high-quality companies with competitive advantages that enable them to deliver solid earnings growth with solid net margin. The strategy’s current portfolio aligns with these principles, with harmonic-weighted averages of 13% for expected earnings growth over 3–5 years and 26% for net margin.

Figure 6 shows how these metrics are broadly aligned with those of peers’ portfolios, exhibiting slightly lower earnings growth but higher net margin. While the portfolios have broadly similar financial profiles, their resilience to adverse shocks from a subset of holdings may vary significantly.

To explore this idea, we reapplied the method previously used to calculate the diversification ratio of holdings. This time, however, the ratio is not derived solely from stock weights, but from each stock’s contribution² to the portfolio’s aggregate earnings growth and net margin.

2. Mathematically, it consists in computing the inverse of the sum of squared contributions, where each contribution is defined as the product of a stock’s weight and its level of earnings growth and net margin.

Figure 7 shows that Polen has the most diversified drivers of both earnings growth and net margin. In other words, it has the potential to be significantly less affected than others if a few holdings were to miss their financial targets.

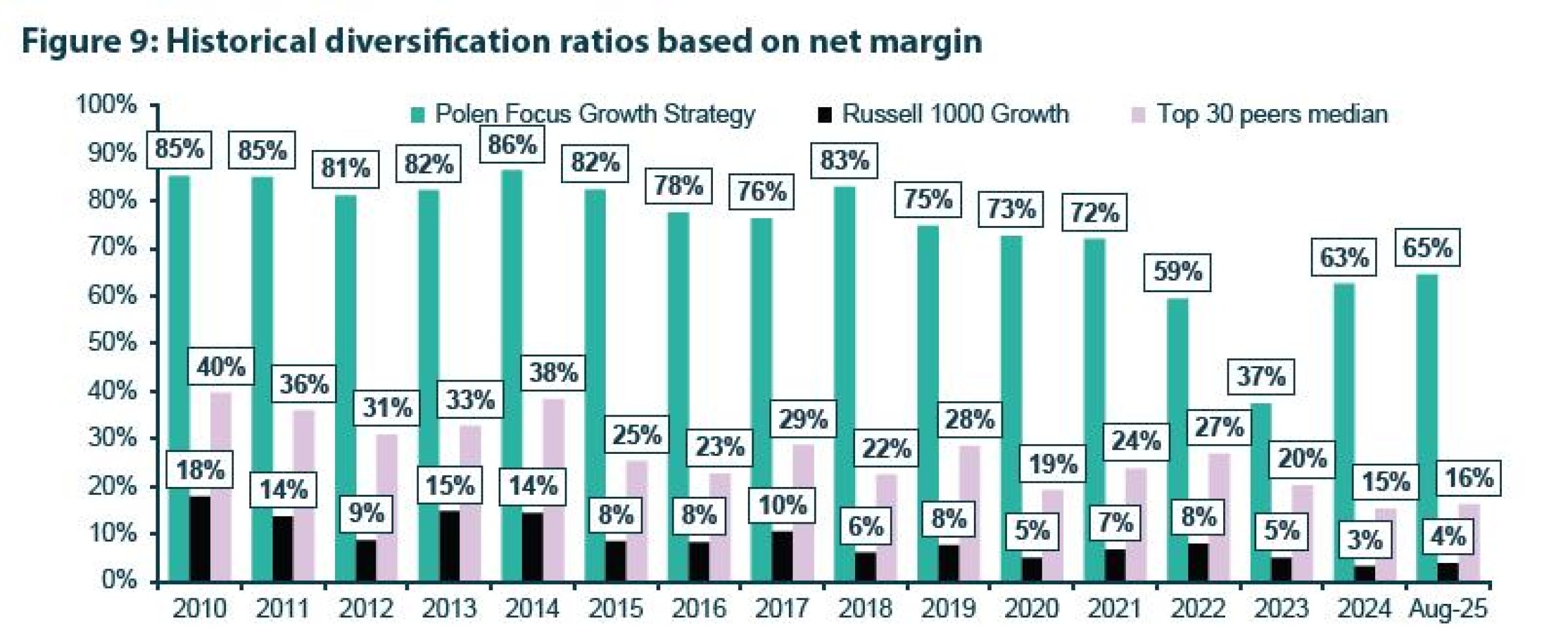

Polen has consistently and successfully maintained this diversified approach. Historical portfolios have demonstrated markedly greater robustness – as measured by diversification ratios of both earnings growth (see Figure 8) and net margin (see Figure 9) – than those of its peer group and the broader market.

Differentiated portfolio structure grants it meaningful diversification strength

This analysis has so far established that Polen’s approach relies on more balanced growth drivers than its peers. The next step is to determine how this positioning influences the portfolio’s diversification power. The most straightforward way to determine how distinct a portfolio is from its peers is to compare active share levels relative either to a common benchmark or to the peer group average portfolio. Figure 10 shows how Polen’s strategy has the greatest differentiation in terms of weight allocation across the peer group.

While a high active share may suggest strong portfolio differentiation, this requires further analysis. Indeed, its impact on active risk can be limited if the underweight and overweight exposures are closely correlated — for example, replacing Coca-Cola with PepsiCo. To this end, we calculated the performance of all portfolios over the past 52 weeks, assuming that their latest allocations remained unchanged throughout the period. This methodology yields a more forward-looking perspective than traditional track record analyses, which rely on historical allocations and offer a backward-looking view of portfolio behaviour. From these simulations, we derived the specific – or active – volatility of each fund, defined as the level of volatility not explained by its exposure to the benchmark. We then calculated, for each fund, the ratio of specific volatility to overall volatility.

As Figure 11 shows, the Polen strategy has by far the highest level of specific volatility within the peer group, both in absolute terms and relative to its overall volatility. This indicates that a larger share of its risk stems from idiosyncratic sources rather than the systematic factor. In turn, this implies that Polen’s strategy is less exposed to common market movements and therefore provides a more substantial diversification benefit within the peer group.

3. Active share is calculated as half the sum of the absolute differences between the portfolio weights and the benchmark weights across all securities.

4. The peer group average portfolio is constructed by averaging the positions of all peer managers.

5. This approach is commonly termed the ‘VaR-based P&L’ framework.

6. Fund Specific Risk = √(Fund Volatility² – Fund’s Beta to Market² × Market Volatility²)

Authored by

Jean Maunoury

Authored by

Luc Dumontier

Authored by

Baptiste Fullana