iMGP Berkshire Dividend Growth ETF Third Quarter 2025 Commentary

12th November, 2025 |

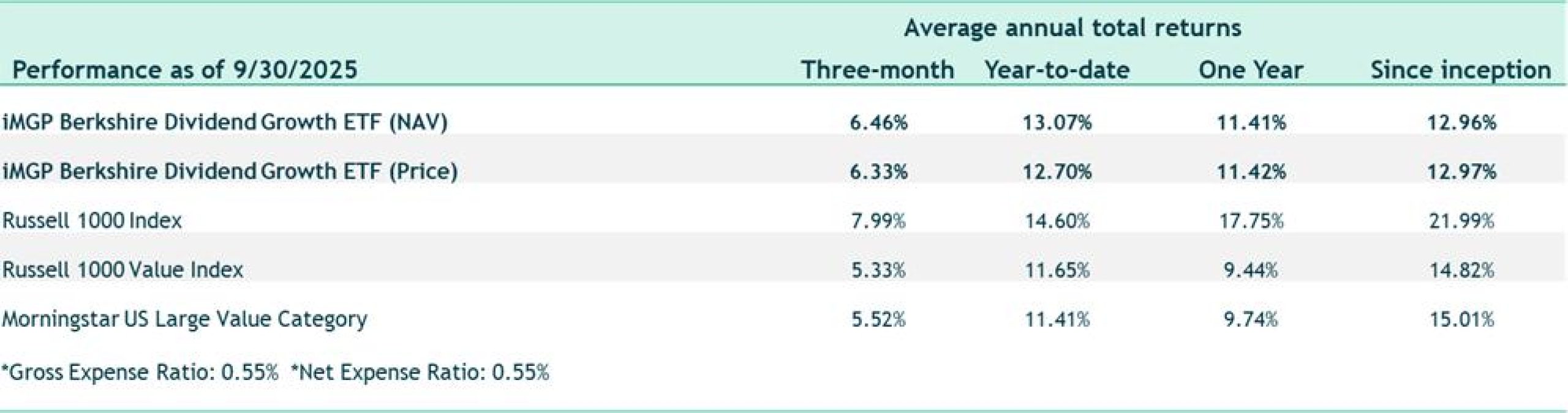

The iMGP Berkshire Dividend Growth ETF Fund returned 6.46% (NAV return) & 6.33% (Market Return) in the third quarter compared to 5.33% for the Russell 1000 Value Index. The Morningstar U.S. Large Value category had a return of 5.52% over the same period.

MSCI index returns source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates, or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Source note: Returns prior to 1999 are the MSCI ACWI ex-US GR index. Returns from 1999 onwards are MSCI ACWI ex-US NR index.

Quietly Compounding: The Best of Both Worlds?

In a world consumed by AI, tariff debates, and rate speculation, it’s easy to lose sight of the quiet compounding power of disciplined dividend investing. However, we continue to believe in its long-term efficacy. Recent market volatility reminds us why the strategy, combined with active management, may provide investors with the best of both worlds.

April reminded us of that discipline and the importance of limiting the downside. While the broader market experienced a sharp dive, our strategy fell much less, echoing the defensive resilience it demonstrated in 2022—when markets dropped more than 20% and select growth names dropped 30–50%. As the growth trade dominates the ether, it’s almost like investors forgot what downside volatility feels like.

Along the way, we made several adjustments—trimming defensive names and selectively adding companies that could be described as more pro-cyclical or slightly higher “beta.” A change in strategy? Hardly. These new names show that our commitment to what we believe are high-quality, cash-rich companies with the potential to compound wealth through dividends remains firmly in place.

By mid-April, markets turned on a dime. The rise—which is nothing short of swift, meteoric, and historic—again proves just how difficult it is to time markets with precision. Quiet compounding through tumult and waiting patiently for the upswing is more our style. This rapid 30%+ climb off the bottom ranks among the quickest advances of that magnitude since 1950 (source: CapTrader, “Record Rally in the S&P,” July 2025).

We observed that our proactive April changes, along with powerful advances in several of our core holdings, allowed the portfolio to participate meaningfully in this sharp rebound. As big a bounce as growth or AI names? No. But our advance reminds us that limiting the downside and attractive upside need not be mutually exclusive.

Behind the Numbers

We see money center banks and big-cap tech as having provided clear tailwinds. Money center banks are thriving, as the benefits of their diverse business models are on full display. Loan growth hasn’t quite hit escape velocity yet, but their capital markets business has. Our “older” tech companies — those with notable free cash flow and reasonable valuations — are thriving. Our newest purchase, Dell, has positioned itself to participate in AI — but owning it comes at a fraction of the valuation, and in our view, provides meaningful dividend growth potential versus the rest of the space. AbbVie, TE Connectivity, and Norfolk Southern are other long-term holdings contributing meaningfully to recent results.

On the other hand, staples have underperformed—particularly General Mills and Pepsi. A general preference for riskier companies has consumer staples lagging a white-hot market. Inflation, GLP-1 drugs, and changing consumer tastes are headwinds for “Big Food” companies. Energy-related issues are having a “so-so” year, but even in these pockets of weakness, we see attractive yields, ample free cash flow, and potential opportunities to capitalize on economic recovery.

Outlook

Economic and market conditions today feel “Goldilocks,” but prices already reflect much of that optimism. An ever-climbing market demonstrates investors are acting as if there is little to worry about—or are happy to shake off any bad news.

But it’s usually the lack of fear, coupled with high prices, that sets investors up for either poor forward returns at best or, worse, a meaningful correction. The S&P 500 P/E? 22.65x. The Technology sector sports a P/E over 30x and represents a whopping 35% of the index. An equal-weight S&P sits at a more moderate 17.63x, suggesting pockets of opportunity remain in a wider range of stocks outside the largest weightings of the S&P. (Source: Bloomberg 9/30/2025)

Our strategy may be built for environments like these. We see it continuing to demonstrate resiliency, quiet yet attractive dividend compounding, and appealing upside. The best of both worlds? Maybe. Berkshire Dividend Strategy will actively work to find those opportunities. With a disciplined focus on dividend growth, quality, and sensible valuation, we hope the strategy would continue to quietly compound wealth over time — and remind clients why they own it in the first place.

| By Sector | BDVG |

| Information Technology | 20.0% |

| Industrials | 18.2% |

| Finance | 17.4% |

| Consumer Staples | 11.5% |

| Health Care & Pharmaceuticals | 10.1% |

| Energy | 7.4% |

| Consumer Discretionary | 7.2% |

| Utilities | 3.1% |

| Materials | 3.0% |

| Real Estate | 1.4% |

| Cash | 0.8% |

| Total | 100.0% |

| By Market Cap | BDVG |

| Large Cap | 73.7% |

| Mid Cap | 24.3% |

| Small Cap | 2.0% |

| Total | 100.0% |

| By Region | BDVG |

| US Equities | 93.2% |

| Developed International Equities | 6.8% |

| Equities | 0.0% |

| Total | 100.0% |

The funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The statutory and summary prospectuses contain this and other important information about the investment company, and it may be obtained by calling 1-800-960-0188, or visiting imgpfunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Past performance does not guarantee future results.

The fund will invest in foreign securities. Investing in foreign securities exposes investors to economic, political and market risks and fluctuations in foreign currencies. Though not a small-cap fund, the fund may invest in the securities of small companies. Small-company investing subjects investors to additional risks, including security price volatility and less liquidity than investing in larger companies. Investments in emerging market countries involve additional risks such as government dependence on a few industries or resources, government-imposed taxes on foreign investment or limits on the removal of capital from a country, unstable government and volatile markets. A value investing style subjects the fund to the risk that the valuations never improve or that the returns on value equity securities are less than returns on other styles of investing or the overall stock market.

The MSCI EAFE Index measures the performance of all the publicly traded stocks in 22 developed non-U.S. markets

The MSCI EAFE Value Index captures large and mid-cap securities exhibiting overall value style characteristics across Developed Markets countries around the world, excluding the US and Canada. With 482 constituents, the index targets 50% coverage of the free float-adjusted market capitalization of the MSCI EAFE Index.

The MSCI World Growth Index captures large and mid-cap securities exhibiting overall growth style characteristics across 23 Developed Markets countries.

The MSCI World Value Index captures large and mid-cap securities exhibiting overall value style characteristics across 23 Developed Markets countries. With 848 constituents, the index targets 50% coverage of the free float-adjusted market capitalization of the MSCI World Index.

Each Morningstar Category Average represents a universe of Funds with similar investment objectives.

You cannot invest directly in an index.

Book value is the net asset value of a company, calculated by subtracting total liabilities from total assets.

Market capitalization (or market cap) is the total value of the issued shares of a publicly traded company; it is equal to the share price times the number of shares outstanding.

Price to earnings ratio (P/E Ratio) is a common tool for comparing the prices of different common stocks and is calculated by dividing the current market price of a stock by the earnings per share. Similarly, multiples of earnings and cash flow are means of expressing a company’s stock price relative to its earnings per share or cash flow per share, and are calculated by dividing the current stock price by its earnings per share or cash per share. Forecasted earnings growth is the projected rate that a company’s earnings are estimated to grow in a future period.

The 10-year Treasury yield is the current rate Treasury notes would pay investors if they bought them today. The 10-year Treasury yield is closely watched as an indicator of broader investor confidence.

Yield Curve: A line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates. The most frequently reported yield curve compares the three-month, two-year, five-year and 30-year U.S. Treasury debt. The curve is used to predict changes in economic output and growth.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

Diversification does not assure a profit nor protect against loss in a declining market.

iM Global Partner Fund Management, LLC has ultimate responsibility for the performance of the iMGP Funds due to its responsibility to oversee the funds’ investment managers and recommend their hiring, termination, and replacement.

The iMGPFunds are distributed by ALPS Distributors, Inc. LGE000517 exp. 3/31/28