Persian Gulf – Moving from event risk to duration risk

16th March, 2026 | Insight Article Macro & Markets

| As the conflict in the Persian Gulf enters its third week, investor focus is beginning to shift from event risk to duration risk. Simply put, the longer the conflict persists, the greater the potential damage to the global economy.

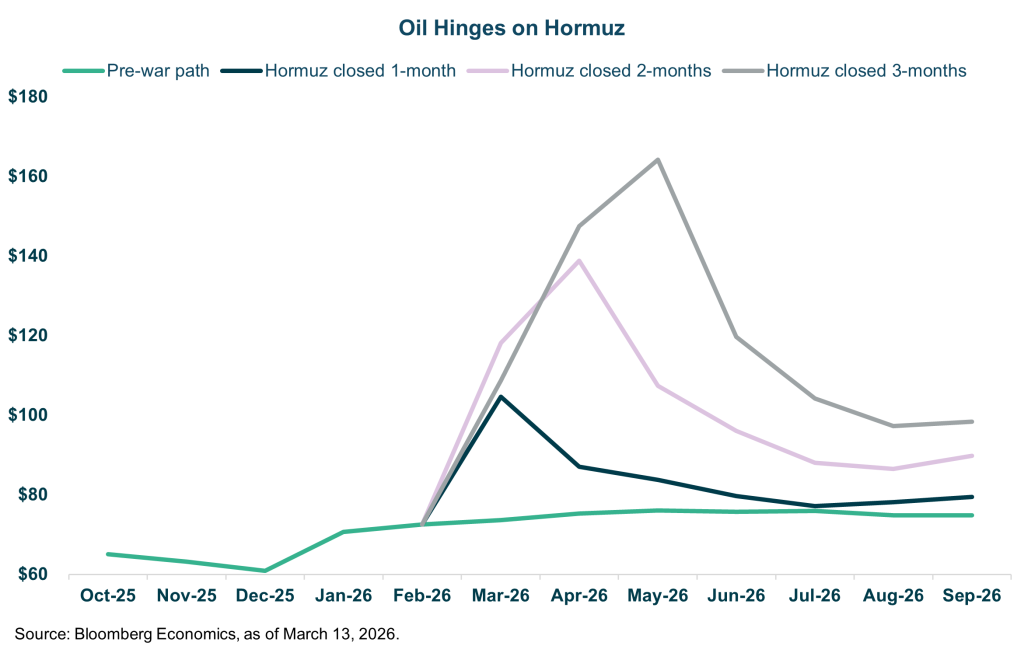

In contrast to predictions from President Trump that the conflict could end quickly, Iran’s new Supreme Leader, Mojtaba Khamenei, has taken a more confrontational stance. In his first public remarks since the escalation, he stated that the Strait of Hormuz should remain closed and suggested that Tehran could open additional fronts if the attacks continue. The implications for energy markets are significant. According to Bloomberg Economics Brent Crude Oil could trade around $105/barrel if the Strait of Hormuz remains closed for one month. Should the disruption extend to three months, prices could rise as high as $164/barrel – levels that would likely have a material impact on global economic growth.

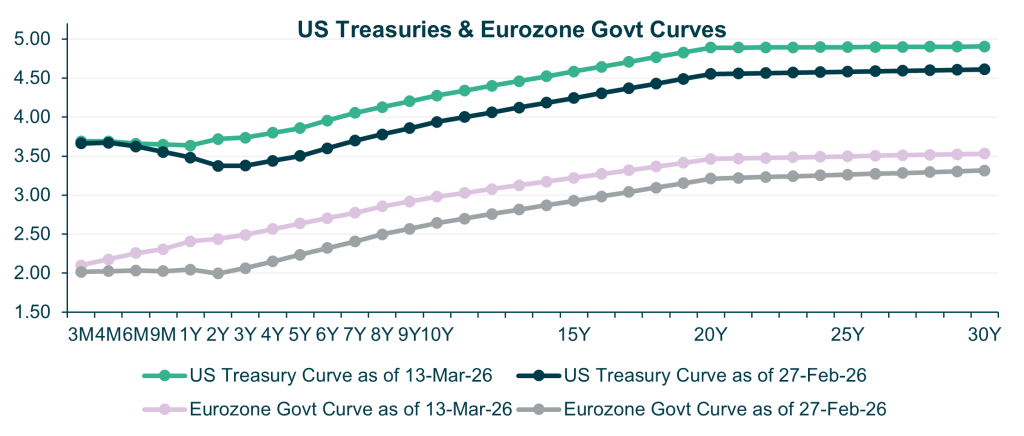

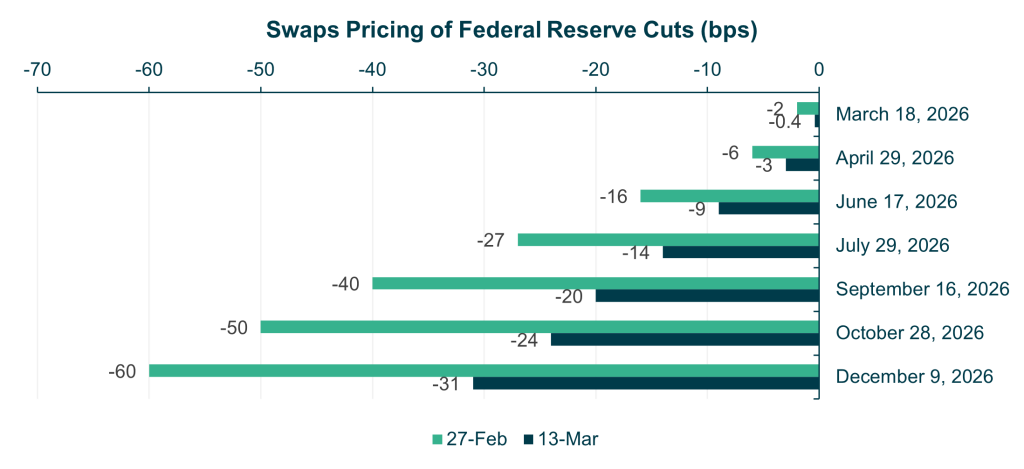

In response, the International Energy Agency (IEA) has authorised a record 400-million-barrel release from emergency reserves, while the U.S. has temporarily allowed the sale of previously sanctioned Russian Oil in an attempt to moderate prices. Although both measures demonstrate awareness of the risk posed by elevated energy prices, neither is sufficient to replace the 20 million barrels of oil which transit the Strait of Hormuz each day. Financial markets have already begun to price in the implications of higher energy prices. In March, yields on both the 10-year U.S. Treasury bonds and Eurozone government bonds have risen by more than 30 basis points, pushing bond prices down and decreasing the odds of near-term interest rate cuts by the Federal Reserve.  Source: Bloomberg, iM Global Partner as of 13 March 2026.  Source: Bloomberg, iM Global Partner as of 13 March 2026

At this stage of the conflict, the only certainty remains uncertainty. We do not believe a continued conflict is in the interest of either the U.S. or Iran; however, at the time of writing there does not seem to be any obvious off-ramp from the conflict. In times of market volatility, the value of diversifying and defensive holdings becomes key for investors. This is particularly relevant given the asymmetrical nature of investment losses: a 20% decline requires a 25% gain simply to return to the starting point. As a result, the ability of a portfolio to weather market volatility is crucial. Avoiding large drawdowns can be just as powerful for long-term wealth creation as capturing all the upside in bull markets. Strategies with superior upside/downside capture ratios can help smooth the return profile of a portfolio and reduce the magnitude of losses during difficult market environments. This is where equity strategies managed with a defensive approach and high-quality fixed income allocations can play a vital role in portfolio construction. Defensive equity strategies, such as dividend-growth approaches focused on high-quality companies trading below intrinsic value, can help limit drawdowns during periods of market stress. Similarly, credit-focused fixed income strategies aim to identify undervalued corporate bonds through disciplined fundamental analysis, helping provide resilience when markets become more volatile. By helping preserve capital and moderate drawdowns, defensive equity and resilient fixed income strategies can support a more consistent path toward long-term investment objectives. |

This document is provided by iM Global Partner Fund Management, LLC (“iMGPFM”) for informational purposes only and no statement is to be construed as a solicitation or offer to buy or sell a security, or the rendering of personalized investment advice. There is no agreement or understanding that iMGPFM will provide individual advice to any investor or advisory client in receipt of this document. Certain information constitutes “forward-looking statements” and due to various risks and uncertainties actual events or results may differ from those projected. Some information contained in this report may be derived from sources that we believe to be reliable; however, we do not guarantee the accuracy or timeliness of such information. Past performance may not be indicative of future results and there can be no assurance the views and opinions expressed herein will come to pass. Investing involves risk, including the potential loss of principal. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made. Indexes are unmanaged vehicles that do not account for the deduction of fees and expenses generally associated with investable products. For additional information about iMGPFM, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website (adviserinfo.sec.gov) and may otherwise be made available upon written request.