Why European High Yield Now

23rd April, 2026 | Fixed Income

European high yield has undergone a quiet but profound transformation. Once a niche segment, it is now a broad, liquid and increasingly resilient market capable of playing a core role in diversified portfolios.

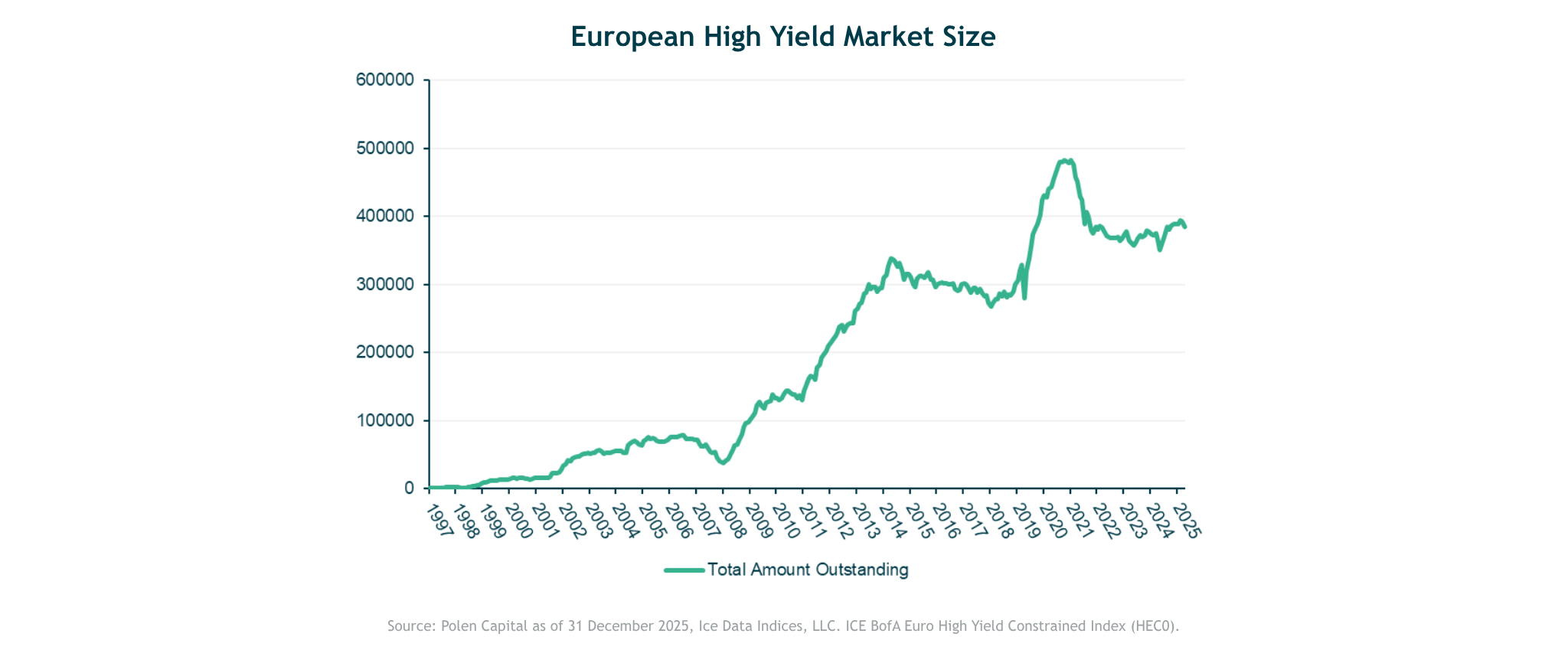

Over the past two decades, the market has expanded from approximately €66bn to nearly €400bn. The number of issuers has more than doubled, while the share of higher-quality BB-rated bonds has risen from around 40% to over 70%. The result is a deeper, more diversified and structurally stronger asset class than commonly assumed.

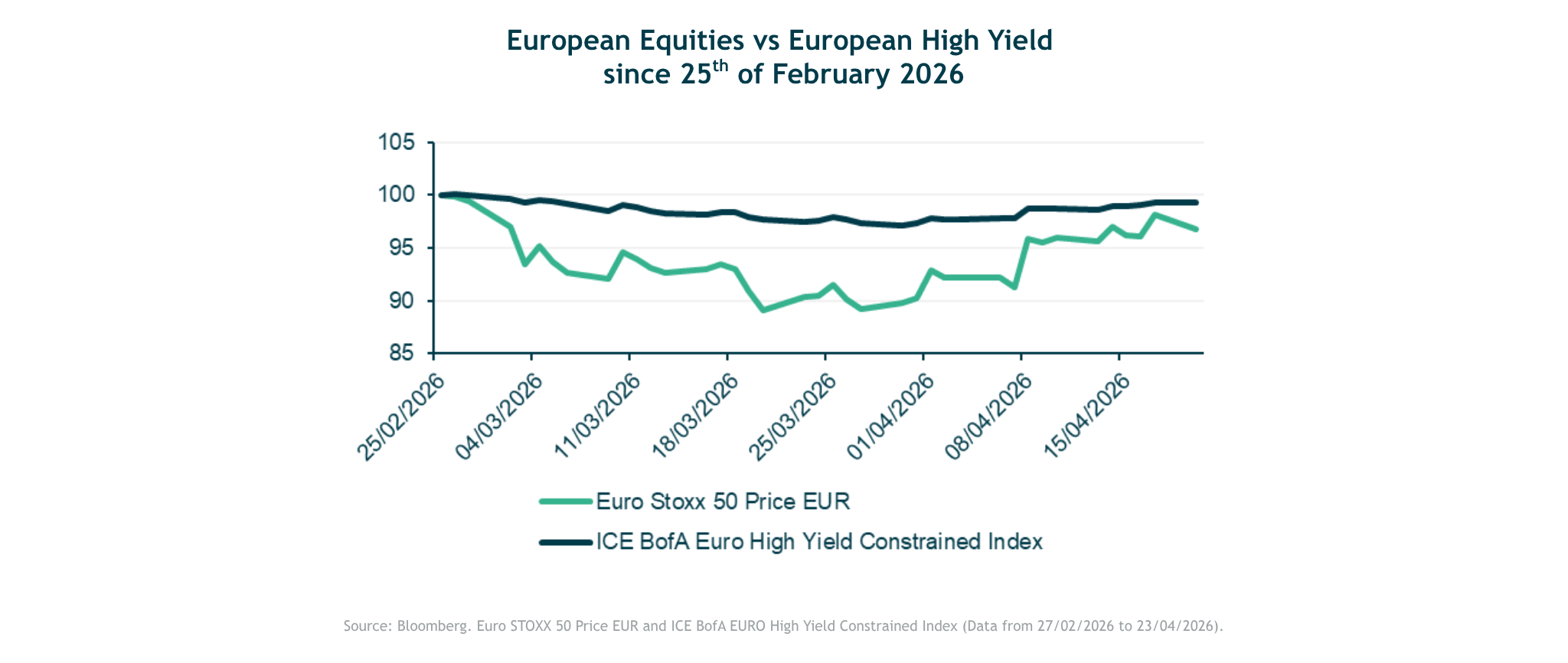

Recent market episodes highlight this evolution. During the 2025 “Liberation Day” drawdown, European equities fell by more than 13% peak-to-trough, while European high yield declined by only around 2.4%. A similar pattern emerged in early 2026, with equities down over 9% versus a modest 2% move in high yield.

This relative resilience is not coincidental.

In combination, these features help limit drawdowns and stabilise returns during periods of stress.

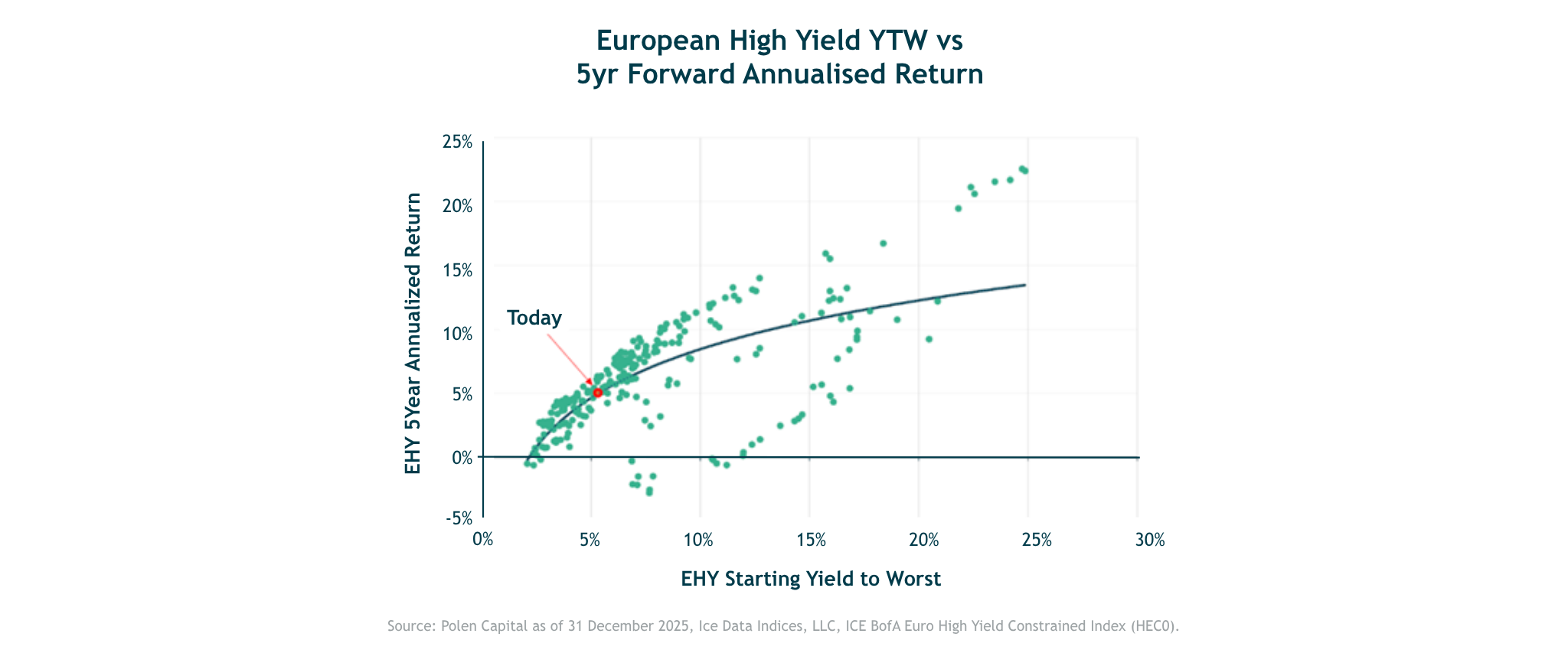

Starting yield has historically been one of the most reliable predictors of long-term returns in high yield markets. When investors enter at higher yield levels, subsequent five-year returns have typically been stronger.

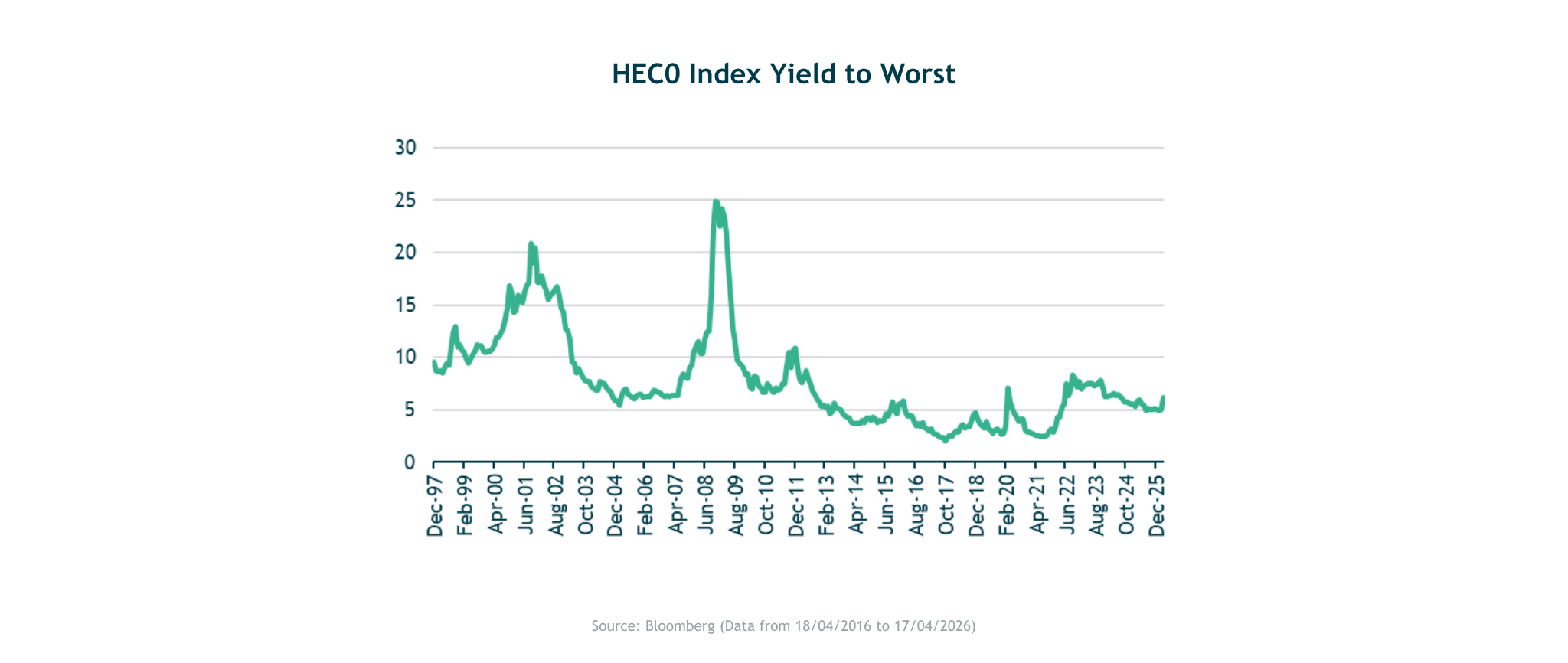

Today, yields remain compelling. The European high yield index offers levels close to the mid-5% range—around 100 basis points above its 10-year average. For active managers able to selectively allocate to single-B bonds while controlling risk, portfolio yields can reach the mid-6% range.

Importantly, this income has historically provided a strong cushion against default risk over time. Over the past two decades, European high yield has consistently delivered higher total returns than investment grade credit, with spread carry acting as a durable return driver.

Breakeven analysis reinforces this point: yields would need to rise materially before returns turn negative over a one-year horizon, reflecting both strong carry and modest duration risk.

The combination of structural market improvement, attractive starting yields, and demonstrated resilience makes a compelling case for European high yield today.